Clients

Clients

Processes

Processes

Blog

Blog

Ten years back, no one could have predicted Blockchain to be the next predominant technology that would forever change the landscape of how businesses operate. Fast forward, and today blockchain technology has become synonymous with success across major industries.

Although a complex concept even more complicated to implement effectively in a business environment, it has enabled companies to make strides in optimizing their business processes so much that it appears to be setting new standards in many industries.

It can be used as a conduit to resolve many leading business risks. One is data protection - Data is becoming increasingly difficult to protect, and the traditional methods of cybersecurity have proven ineffective and costly.

This is where blockchain shines brightest as it provides an alternative to traditional security measures and has proven more effective and sustainable.

This technology enables transactional information to be stored across the decentralized network providing an architecture that is less susceptible to cyber attacks without the involvement of third parties. The difference between traditional databases and blockchains is in the structure.

What makes blockchain unique is how data is collected and stored. Data is stored in blocks and linked to the previous blocks on the chain - hence the term - Blockchain. Once each block is minted, the information inside is irreversible, given an exact timestamp, and added to a chain.*Minting a block = validating information, creating a new block, and recording that information into the blockchain

When browsing the different blockchains, users might experience a difference in structure and details available which may be due to the different types of blockchains, some of which are:

So far, we’ve covered: high level impact of blockchain on business, basics of blockchain and types of blockchain, so the eventual question is *How Can Blockchain Technology Improve My Business?

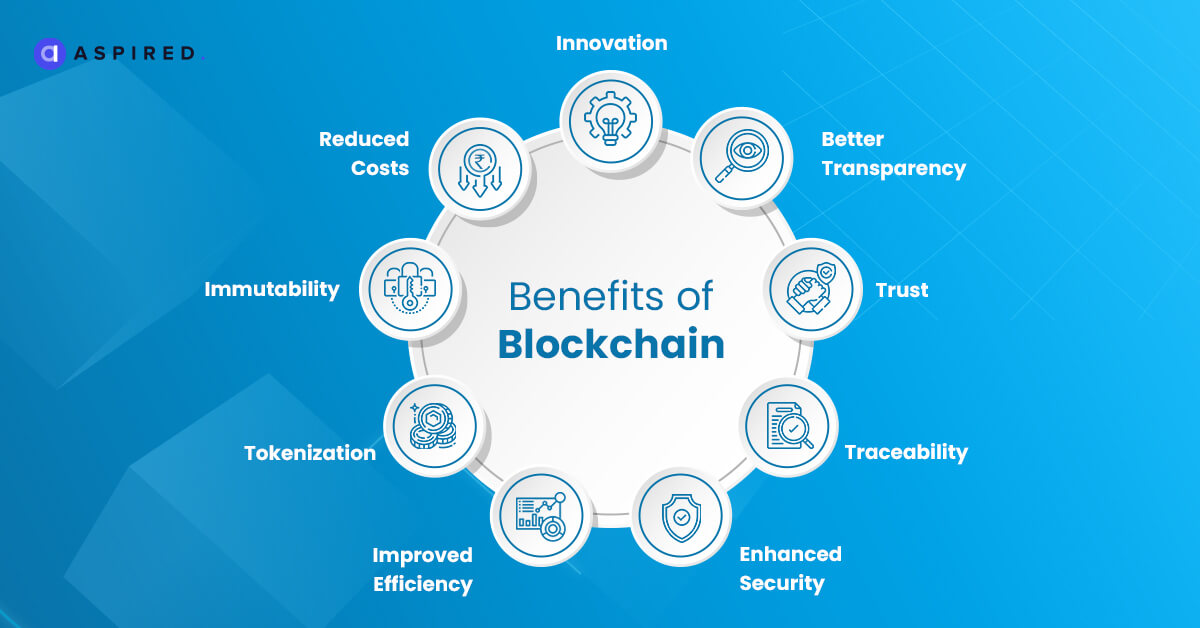

First off, great question! There's no simple answer - which is a good thing. It depends on your business goals (short & long term), data-culture and more. To help you understand how blockchain can help your business today - let’s review what benefits it offers:

Before we review the benefits, it is worth noting that Blockchain is a collaborative technology which aims to lower the ‘Cost of Trust’ while offering transparency and higher investment returns. This, in turn, reduces long-term upkeep costs for businesses.

With the in mind, the benefits include:

Although a complex concept even more complicated to implement effectively in a business environment, it has enabled companies to make strides in optimizing their business processes so much that it appears to be setting new standards in many industries.

It can be used as a conduit to resolve many leading business risks. One is data protection - Data is becoming increasingly difficult to protect, and the traditional methods of cybersecurity have proven ineffective and costly.

This is where blockchain shines brightest as it provides an alternative to traditional security measures and has proven more effective and sustainable.

A Quick Intro to Blockchain Technology

In short, blockchain technology is, at its core, a database structure that is hosted and maintained by a network of independent nodes, as opposed to a centralized ecosystem. *Nodes = individual computers on the same networkThis technology enables transactional information to be stored across the decentralized network providing an architecture that is less susceptible to cyber attacks without the involvement of third parties. The difference between traditional databases and blockchains is in the structure.

What makes blockchain unique is how data is collected and stored. Data is stored in blocks and linked to the previous blocks on the chain - hence the term - Blockchain. Once each block is minted, the information inside is irreversible, given an exact timestamp, and added to a chain.*Minting a block = validating information, creating a new block, and recording that information into the blockchain

- Data – The information contained in each block

- Nonce – Randomly generated whole number assigned to each block at creation. This number is used only once, hence the name.

- Hash – The hashcode is a reference number generated each time a block is created. It is permanently attached to the nonce, and includes the hashcode from the previous block.

What are the Different Types of Blockchains?

A block explorer (or blockchain explorer) enables users to visualize blocks, and search for real-time & historical information related to blocks, transactions, even addresses, and other blockchain network metrics (e.g., average transaction fees, hash rates, block size, block difficulty) including access to hidden messages.When browsing the different blockchains, users might experience a difference in structure and details available which may be due to the different types of blockchains, some of which are:

- Private and public networks – Private blockchains are best suited for closed networks in organizations as it allows for customizable accessibility and security options. Meanwhile, public networks use an open peer-to-peer network to store data

- Prominent examples of private networks include Quorum, Hyperledger Fabric, and R3 Corda.

- Bitcoin & Ethereum are examples of public networks.

- Federated or Consortium Blockchains – Consortium Blockchains can be considered to be groups of private chains, each owned by individual organizations that have banded together to share data/information to improve workflows, accountability & transparency in a collaborative effort. Private chains are programmed to act in a consortium framework.

- Permissioned Blockchains– Permissioned or Hybrid networks are private chains focused on user authentication and access controls. They offer better security structures for highly-sensitive data-driven projects with increased visibility & control into user-specific transactions.

So far, we’ve covered: high level impact of blockchain on business, basics of blockchain and types of blockchain, so the eventual question is *How Can Blockchain Technology Improve My Business?

First off, great question! There's no simple answer - which is a good thing. It depends on your business goals (short & long term), data-culture and more. To help you understand how blockchain can help your business today - let’s review what benefits it offers:

Before we review the benefits, it is worth noting that Blockchain is a collaborative technology which aims to lower the ‘Cost of Trust’ while offering transparency and higher investment returns. This, in turn, reduces long-term upkeep costs for businesses.

With the in mind, the benefits include:

- Increased Security One of the forefront features of a blockchain is its inherent security capabilities, mainly derived from the decentralized data storage structure, data immutability & finality. In other words, once done - no changes - ever! An example of this could be a blockchain wallet, when performing a transaction with a digital wallet, a unique signature is required and without it the transaction can’t be performed. However, once the transaction is performed, it is permanently recorded in a block with all relevant details, verified by & stored on all nodes on the network - making it impossible to hack.

- Decentralization The decentralized nature of Blockchain makes it a far more trust-worthy storage system compared to traditional ecosystems. It is because the vast majority of nodes verifies each transaction before accepting it on the blockchain rather than trusting one-third party to take that responsibility on (and submit to their terms of use). This enables blockchain-powered businesses to be more alluring to the new-age consumers as they offer a trust-less, faster, more accessible & transparent system.

- Automation Automation and Blockchain go hand-in-hand, which means a huge-upside for businesses when considering optimizing current processes that are otherwise time consuming and costly. With smart contracts, businesses can employ seamless automation on nearly every aspect of business as long as the contracts are well-planned and executed. Outcome-based transactions are carried out in a matter of seconds, and each transaction is traceable, all while ensuring transparency & minimizing fraud as it requires no manual input.

- Reduced Cost Due to their efficiency in processing transactions, blockchain characteristics make it exceptional for reducing manual tasks. With Blockchains, organizations can easily audit and amend data to streamline processes, clearing and settlements. Businesses benefit by circumventing third-parties to carry out these otherwise costly tasks.

- Bottom Line Although blockchain technology has been available for some time now, businesses across all industries are beginning to realize its value, especially regarding data security which makes it a great alternative to traditional databases. By nature, it has fewer vulnerabilities and works well with automation while providing transparency. All-in-all, blockchain technology enables businesses to be leaner and more efficient as it eliminates the need to perform monotonous and mundane tasks while fueling growth opportunities.